Oil prices soared more than 10% in hectic trading on Monday as the risk of a U.S. and European ban on Russian product and delays in Iranian talks triggered what was shaping up as a major stagflationary shock for world markets.

The euro extended its slide and commodities of all stripes were on the rise as the Russian-Ukraine conflict showed no sign of cooling. Russia calls the campaign it launched on Feb. 24 a “special military operation”, saying it has no plans to occupy Ukraine.

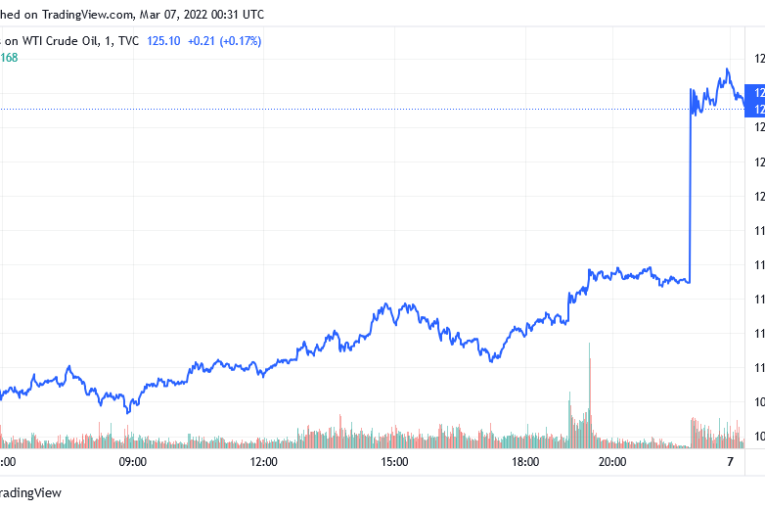

Brent was quoted $12.73 higher at $130.84, while U.S. crude rose $9.92 to $125.60.

The potential blow to global economic growth saw S&P 500 stock futures drop 1.1%, while Nasdaq futures shed 1.4%.

Futures for Japan’s Nikkei were trading around 300 points below the cash close on Friday, while U.S. Treasury futures jumped 10 ticks as investors sought safe-havens.

Having climbed 21% last week, Brent crude was further energised by the risk of a ban of Russian oil by the United States and Europe.

“If the West cuts off most of Russia’s energy exports it would be a major shock to global markets,” said BofA chief economist Ethan Harris.

He estimates the loss of Russia’s 5 million barrels could see oil prices double to $200 a barrel and lower economic growth globally.

And it is not just oil, with commodity prices having their strongest start to any year since 1915, says BofA. Among the many movers last week, nickel rose 19%, aluminium 15%, zinc 12%, and copper 8%, while wheat futures surged 60% and corn 15%.

That will only add to the global inflationary pulse with U.S. consumer price data this week expected to show annual growth at a stratospheric 7.9%, and the core measure at 6.4%.

All of which complicates the policy picture for the European Central Bank when it meets this week.

“Given the potential for stagflation is very real, the ECB is likely to maintain maximum flexibility with its asset purchase programme at 20 billion euros through Q2 and potentially beyond, thus effectively pushing out the timing of rate hikes,” said Tapas Strickland, an economist at NAB.

“Higher CPI forecasts, though, mean rate hikes will be needed on the horizon.”

The near-term prospect of a more dovish ECB combined with safe-haven flows to drive German 10-year bond yields down a huge 32 basis points last week, while U.S. yields dropped 23 basis points to 1.738%.

With the outlook for European growth darkening, the single currency took a beating and fell 3% last week to its lowest since mid-2020. It was last down 0.6% at $1.0864 and risked testing its 2020 trough around $1.0635.

The dollar was broadly firmer, supported in part by a strong payrolls report which only reaffirmed market expectations for a rate hike from the Federal Reserve this month. The dollar index was last at 98.812 having climbed 2.3% last week.

Gold benefited from its status as one of the oldest of safe harbours and was last up 0.7% at $1,983 an ounce.

(Reporting by Wayne Cole; Editing by Sam Holmes)

You can read more of the news on source